Rates, Fed undecided on next moves: the outcome of the December FOMC meeting is less predictable than those in September and October. What do analysts predict?

Fed rates have a significant impact on financial markets: investors, aware of the importance of interest rates, try to anticipate the decisions of the FOMC (Federal Open Market Committee) to position themselves in the best possible way. Compared to the last two meetings, where the outcomes were practically a foregone conclusion, the December meeting presents numerous unknowns: what is the most likely outcome?

What happened at the last FOMC meeting?

On 28-29 October, the Fed met at its headquarters in Washington to discuss the macroeconomic situation and decide what to do about interest rates: the Council, with ten votes in favour out of twelve, opted for a 25 basis point cut, lowering rates by 0.25% to a range between 3.75% and 4%.

The outcome, as we anticipated, was widely expected and already discounted by the markets, which had been growing for weeks – except for the halt on 10 October, when Trump announced 100% tariffs on China.

But it was the press conference following the meeting that was the real key moment. Here, Federal Reserve Chairman Jerome Powell, in listing the reasons behind the cut, made a very significant statement: “A further cut in benchmark interest rates at the December meeting is not a foregone conclusion, quite the contrary.” Markets in chaos.

Since Powell uttered those words until now – that is, at the time of writing – the major stock indices have entered a phase of severe difficulty, but then they rebounded and are now flat.

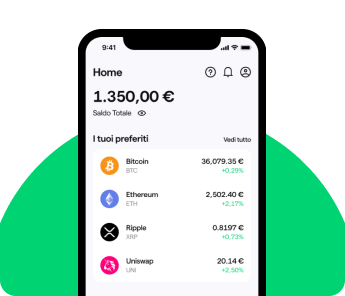

The crypto market has also taken a hit, of course, with Bitcoin down 16.8 percentage points since 29 October and Ethereum down almost 20,6. Overall, since that fateful day, the total market cap has fallen by £600 billion, from £3.7 trillion to £3.11 trillion.

Fed, shutdown and block on the publication of macroeconomic data

During that press conference, Powell responded to questions from journalists about the shutdown’s impact on federal activities. In particular, curiosity focused on the stance the Fed might take at the next FOMC meeting, in a context of almost total absence of data crucial for analysing the macroeconomic scenario.

Powell himself had already mentioned the difficulties of the moment, stating that “although some important data has been delayed due to the shutdown, the public and private sector data that remains available suggests that the outlook for employment and inflation has not changed much since our September meeting“.

On this issue, however, the most interesting response came from the Fed Chairman to Howard Schneider of the well-known Reuters news agency. The journalist rightly asked him whether the lack of key information, such as inflation or employment, could have led members of the US central bank to “make monetary policy based on anecdotes”, i.e. qualitative data – such as personal opinions – rather than economic models based on quantitative data.

Powell initially stated that ‘this is a temporary situation’ and that ‘we will do our job‘. He then went on to say, ‘If you ask me whether it will affect the December meeting, I’m not saying it will, but yes, you can imagine… what do you do when you’re driving in fog? You slow down.

In short, the latest FOMC press conference presented us with a Jerome Powell who appeared even more cautious than the classic “we’ll wait and see” approach that characterised the first six months of 2025. A determined Jerome Powell, who wants to see his task through to the end, even though he will leave the top job in May 2026 to make way for the new Fed Chair.

Fed rates: what do analysts and prediction markets forecast?

Here too, the question is entirely open. The most authoritative voices are divided into two camps: a 25-basis-point cut versus no change (rates unchanged). There is, of course, no mention of a 50 basis point cut.

The first faction, in favour of a quarter-point cut, is leveraging the weakness of the labour market, particularly the slowdown in hiring: in a Reuters poll of 105 economists, 84 bet on a quarter-point cut, while the remaining 21 chose the No Change option.

In particular, Abigail Watt, an economist at UBS, justified her vote to Reuters by stating that ‘the general feeling is that the labour market still appears relatively weak, and this is one of the key reasons why we believe the FOMC will cut in December‘. Watt goes on to say that she would change her opinion if data were released that ‘contradicted this sense of weakness‘.

The second faction, those in favour of unchanged rates, instead takes as its main argument Powell’s words quoted above: “the outlook for employment and inflation has not changed much since our September meeting“.

For example, Susan Collins, head of the Boston Fed, is of this opinion and believes that a third consecutive cut could fuel inflation at a time when the impact of Trump’s tariffs remains unclear. Specifically, she told CNBC that “it will probably be appropriate to keep interest rates at their current level for some time to balance the risks to inflation and employment in this environment of high uncertainty“.

Interest rates, according to the FedWatch Tool and Polymarket

FedWatch is a financial tool provided by the CME (Chicago Mercantile Exchange) that calculates the implied probabilities of future Federal Reserve interest rate decisions. Why ‘implied’? Because it deduces probabilities from the market prices of 30-day Federal Funds futures rather than from explicit opinions.

In simple terms, FedWatch reports market expectations by looking at investors’ portfolios. If it says ‘80% probability of a cut’, it means that 80% of the money invested in the market today is betting on a cut. Currently, according to this tool, a 25 basis point cut is 89,6% likely, while No Change is 10,4%.

According to the most famous prediction market of the moment, Polymarket, the result is a 25 basis point cut at 97%, No Change at 3%, a 50 basis point cut at 1% and a 25 basis point increase at around 1% – if you are interested in knowing how it works, we have written an Academy article dedicated to Polymarket.

What will the Federal Reserve do?

As we have explained so far, the Fed will have to take a large number of variables into account before its Chairman leaves the room, approaches the microphone and utters the familiar ‘Good afternoon‘.

Related Article

Download the Young Platform app